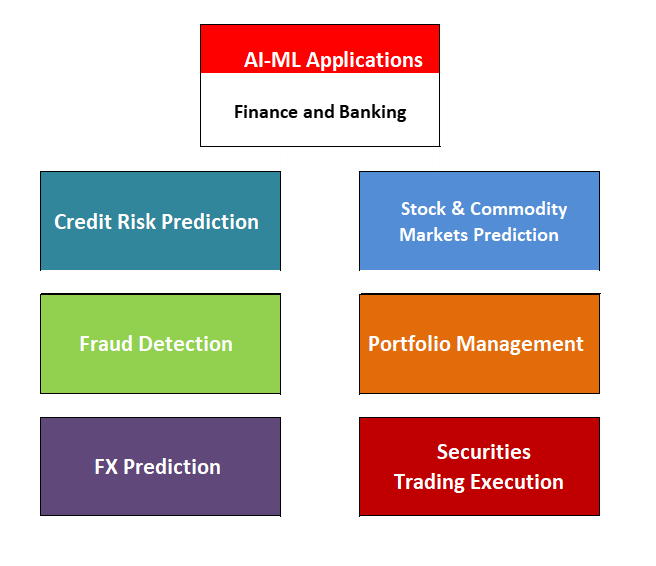

Enabled through advances in Information Technology (IT), Artifical Intelligence (AI) and Machine Learning (ML) find applications across multiple areas of Finance. Today, the availability of machines and algorithms specialised in learning and decision making from data make applications possible that draw insights from complex and high dimensional data. In addition, novel data sources lead to an increase in data complexity whilst providing a lever to usefulness of AI-ML techniques.

Oftentimes calibration of AI-ML algorithms requires to take a large number of parameter and Model configurations into account. As a case in point, calibrations of highly parameterized AI-ML Models require automated finetuning approaches. AI-ML is used across different risk areas whereby the Model applications of AI-ML in Credit Risk merit highlighting due to the significance of this risk area across financial institutions. As a case in point, applications of AI-ML in Credit Risk range from optimizing operational processes for credit lending, increasing prediction accuracy for capital, and enhancing risk-adjusted pricing and borrower risk assessments. In summary, methods and technologies drawn from AI-ML provide effective leverage for identifying, measuring, and mitigating the different risks that that determine business in Finance and Banking.

Disclaimer: The information is provided for mere information purposes as part of this blog. Auriscon Ltd and Auriscon HK Ltd assumes no responsibility or liability for any errors or omissions in the content of this site. The information contained in this site is provided with no guarantees of completeness and accuracy. No liability is assumed by Auriscon for any damages that may occur for external use of information provided herein.

Automation of data processing based on AI-ML technology is a common use case across different application and risk areas. Automation enables the analysis of large quantities of structured and unstructured data whilst reducing labour cost and enhancing response time. Robotic Process Automation (RPA) for instance, used for Business Process Automation (BPA), serves to execute complex tasks and to run processes in any business. Enhancing processes through automation and AI-ML automates complex decision-making tasks and achieves performance with minimized error and cost.

In Credit Risk, improving prediction accuracy and utilizing alternative data sources and real-time data can leverage risk assessments substantially. In the limit, AI-ML technology proves useful to update credit risk assessments on-demand, to continually provide monitoring and to screen borrowers for any deterioration of credit profiles. Credit Management benefits from such enhancements in varous ways, may it me through proactive adjustments in lending standards, the reduction in credit limits, or the detectoin of emerging risk affecting credit portfolio managment.

In Fraud Risk, AI-ML finds application for detection of fraud in transaction processing. Fraud Risk commonly involves many detail steps for data screening, verification of anomalies and ad-hoc investigations, all of which subject ot AI-ML technology and methods.

PD, LGD and Scoring applications in Credit Risk and Lending are increasingly leveraged by AI-ML techniques. This involves Loan Credit applications being subject to automated decision making for discriminating between potential future defaulters and non-defaulters. Various machine learing methods are applied including Logistic Regression, Random Forest, Boosted Trees and SVM.

Ensemble techniques in particular compare favourably to single models. Random Forests fits a large number of trees for prediction, with each tree only using a subset of predictor variables and fitting only a subset of observations. Gradient Boosting Trees is another example for using an ensemble of single models, and often provides superior performance due to combining multiple regression (or classification) trees whilst accounting for non-linear relationships between variables. Other Supervised Learning methods such as Artifical Neural Networks (ANN) are similarly effective. In applicatons of ANN, multi-layer networks are typically used whereby the number of layers used increases until no further improvement in accuracy is detectable.

Alternative data sources can be used in conjuction with AI-ML techniques to overcome the challenge of analyzing credit profiles of corporate start-ups or retail borrowers with limited data history.

Regularization techniques find applications for problems where a large number of variables are involved with significant correlations between pairs of variables unavoidable. For Regression models, Ridge and Lasso are the common techniques applied to ensure unbiased regression results in the presence of many correlated variables. A desirable side effect of Regularization is that regularized models can be expected to better generalize to out-of-sample data.

Demonstrated below an example of using Logistic Regression to Boosted Tree for the purpose of Loan Application scoring

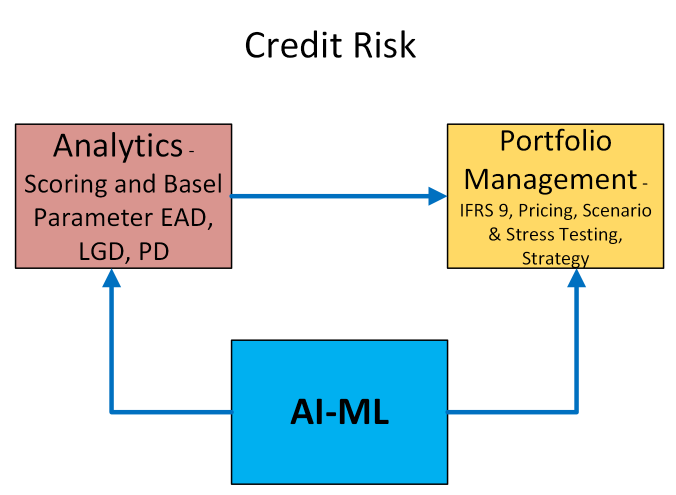

Credit Portfolio Management can use AI-ML techniques for an adaptive balancing of risk and return at portfolio level. At a technical level, AI-ML can support in monitoring the changes in risk factors to timely update factor models to input the rebalancing of credit portfolios. Industry specific risks affected by changing economic conditions can be identified and evaluated in an automated way through scenario analysis and stress testing.

Credit Portfolio Management can use AI-ML techniques for an adaptive balancing of risk and return at portfolio level. At a technical level, AI-ML can support in monitoring the changes in risk factors to timely update factor models to input the rebalancing of credit portfolios. Industry specific risks affected by changing economic conditions can be identified and evaluated in an automated way through scenario analysis and stress testing.

As part of the underwriting process, the way to leverage the process involves the set-up of AI-ML supported automation for data extraction, data integration and data analysis. Alternative data sources identified and used for data extraction provide valuable add-on information. For example, lack of credit information for retail borrowers may be bridged by extracting and analyzing data from utility bills or online shopping behaviour. Determining optimal interest rates and loan terms can be optimally supported by use of AI-ML, leading to a balance of risk and return that can be updated frequently if required.

Customer Churn occurs when bank customers turn away such that the business relationship between a bank and its customers cease. Understanding the drivers of churn and predicting churn based on sutiable AI-ML classification and prediction technqiues is an important aspect that is contributing to the success in portfolio management and customer retention.

→ Tip:Evaluating Portfolio models and analytical approaches for Portfolio management can be a complex task with risks of errors in the evaluation processes. Auriscon supports in identifying sutiable Models and approaches alongside evaluation with analytical assistance provided end-to-end.

Fin-Tech is an industry branch within Finance that provides many examples for a business model that utilized the advantages of digitalization. Various specialized services are provided by the FinTech industry such as robot financial advisors for automated advising and assistance in portfolio management. Other automated services are used for peer to peer lending, crowd funding,and access to trading systeTech ms for a retail clientele.

Large Language Models (LLM) are utilized throughout Finance and Banking and FinTech companies are no exception to this trend. Automating email drafting using LLM leverages artificial intelligence to streamline communication, by generating professionally articulated messages that updates on previous correspondences. Trained to recognize the nuances of different types of emails allow LLM to distinguishing between updates, client inquiries, and requests. Moreover, integration of these LLM systems with existing CRM systems provides a way to access the relevant customer data swiftly, which proves useful for a more engaging and tailored customer experience via email.

→ Tip:Training and validating AI-ML models can be a laborous and complex task with risks of errors in the model development and validation processes. At Auriscon we can help in identifying inconsistencies in the development and validation approach and point to opportunities to enhance model design and validation.

Algorithmic Trading employs strategies developed and applied based on algorithmic and machine learning signals. This approach enables a speedily identification of trading patterns with sufficient accuracy, thereby leading to fast prediction of securities prices and execution on trading decisions.

In the context of securities trading the volatility surface is an important concept for the pricing of options.The volatility surface of an option depends on the time to maturity and the strike price and evolves dynamically through time. Consequently, understanding the dynamics of a volatility surface is prerequesite for effective hedging and pricing. Using Neural Networks enables the modelling of the volatily dynamics without having to resort to complicated and at times slow traditional numerical pricing algorithms.

Generating synthetic data with the same properties as those observed in actual data is a desirable tool for many areas including Finance. Neural Networks in the form of Autoencoders and variations thereof provide the right technique for such a task. Autoencoders are also useful for dimensionality reduction, whereby a large number of features is reduded to a much smaller number of features that possess the same information content.

Fraud Risk, a sub-area of Compliance Risk, is concerned with prevention of money laundering and to establish surveillance over transactions various AI-ML oriented approaches have become established. In Fraud detection AI-ML models learn from identifying patterns of fraudulent transactions. These patterns help to discriminate normalized from fradulent behavior and make it easier to detect suspicious activities, like money laundering or insider trading. Boosted Trees when used for Fraud detection provide an effective approach to account for a large number of features. In Gradient Boosting an ensemble of Trees is used for model fitting, with each iteration a new predictor is fitted to the errors hat remain from the previous sequence of models. Furthermore, Bayesian networks are suitable for anomaly detection since high dimensional data can be dealt with. N.B. Plotting individual variables can reveal simple anomolies but often anomalies are based on the interaction of many variables and hence more complex.

Customer screening is a case in point where AI-ML have been successfully applied. Caveats occur however: due to a large number of false positives produced operators have to process all false positives of an outcome run. Clearly, a business objective in this regards is to minimize false positives and thus reducing operator labour and operational costs involved. Another case in point is Anomaly detection: identifying unusual data for the processing of events or financial transactions can be based on different AI-ML techniques. The outcome is then used for the removal of unusal data (outlier) to ensure that only trusted data is used to feed precition models.

© 2026 Auriscon Ltd. No reproduction without permission. Short excerpts with attribution permitted.